Trader Hub

ST Engineering – Defence and Security Led Earnings Growth

traderhub8

Publish date: Mon, 04 Mar 2024, 11:20 AM

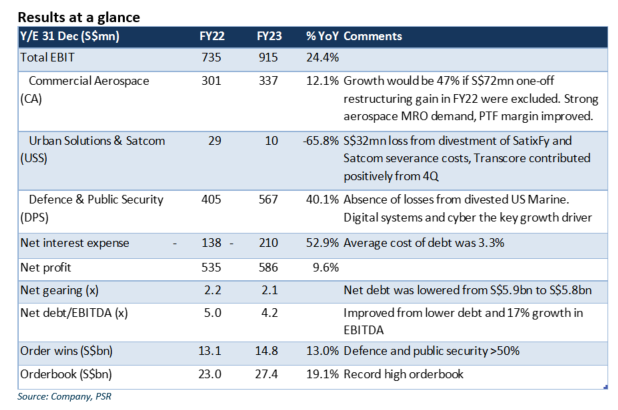

- FY23 net profit was in line with our expectations. Net profit was affected by several one-offs amounting to S$66mn. Excluding these, net profit would have grown by 23.7%.

- Defence and Public Security (DPS) (+40.1% YoY) led earnings growth, with digital sytems and cyber the largest growth engine. Commercial aerospace (CA) grew 47% YoY (excluding one-off items) with increased MRO demand and improved margins from passenger-to-freighter conversions. Urban solutions and Satcom (USS) incurred loss on divestment and severance costs on restructuring. Transcore turned profitable in 4Q23. Orderbook remained strong at S$27.4bn.

- We maintain our FY24e earnings forecast and TP of S$4.50. DPS would remain the key earnings driver in FY24e, underpinned by digital solutions, AI-enabled command and controls, and cybersecurity. Due to recent price appreciation, we downgrade our recommendation to ACCUMULATE from BUY.

The Positives

- Aerospace MRO revenue rose 41%, as demand surged in tandem with recovery in air travel. The passenger-to-freighter conversion business has also scaled the learning curve and is turning profitable. However, commercial aerospace FY23 EBIT margin fell 1.5% pt to 8.6% due to higher manpower costs.

- Defence and public security posted EBIT growth of 40%. Despite the flat revenue, EBIT margin gained 3.8% pt to 13.3% due to better product mix and absence of US Marine losses. The largest sub-segment, digital systems and cyber accounted for 39% of total revenue (FY22:35%).

- Net debt was marginally lower at S$5.8bn (Dec 22: S$5.9bn), but net debt to EBITDA improved to 4.2x, from 5.0x in Dec 22 due to stronger EBITDA. Management remains focused on paring down the debt. The dividend is expected to be maintained at 16 Sct/share.

The Negative

- Restructuring at Satcom and divestment of SatixFY resulted in a S$24mn loss at USS. On a positive note, Transcore turned profitable in 4Q23, and is expected to lift USS’ EBIT from FY24e.

Source: Phillip Capital Research - 4 Mar 2024

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Trade Confidently & Analyze Charts Conveniently - Download VCPlus IOS & Android App Now!

Latest Videos

Apps

Top Articles

1

Collin Seow Remisier Blog

Baker Hughes: Powering Essential Industries and Your Portfolio

2

SGX Market Updates

3

RHB Investment Research Reports

Marco Polo Marine - Higher Capacity To Drive Growth; Maintain BUY

4

SGX Market Dialogues

5

STE's Stocks Investing Journey

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....