Trader Hub

China Aviation Oil – Net Profit and Dividend Beat Expectations

traderhub8

Publish date: Mon, 04 Mar 2024, 11:20 AM

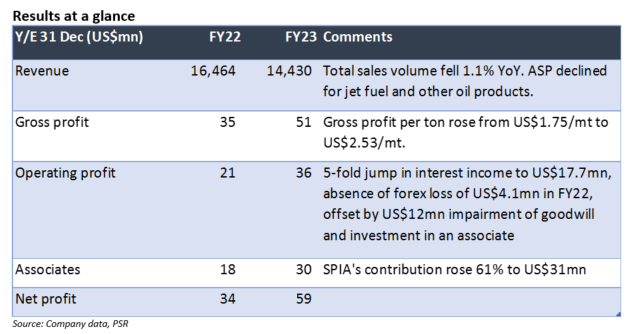

- The results beat our estimates by 22%, due to stronger-than-expected contributions from 33%-owned SPIA.

- Net profit rebounded 75.5% due to 1) stronger demand for jet fuel with borders reopened from early 2023; 2) higher margin per metric ton with increased direct sales with airline customers; and 3) SPIA’s net profit jumping 61% YoY. Net cash at year-end was US$373mn (S$0.623/sh). Full-year dividend was raised to 5.05 Sct (FY22: 1.6 Sct), a yield of 5.4%.

- China’s international air traffic is still at 37% below pre-Covid level. Flights are progressively being restored with further normalization of aviation services. China accounted for 62% of total revenue in FY23.

- Maintain BUY call and raised TP to DCF-derived TP to S$1.05 (prev. S$1.01). We lifted our FY24e net profit estimates by 17% to factor in improved gross margin.

The Positives

- Gross profit per metric ton jumped to US$2.53 in FY23 (FY22 US$1.75/mt). The margin in 2H23 was 145% higher YoY at US$3.78/mt. This was achieved through engaging in more end-to-end sales, sourcing products from refinery for delivery to the airline customers. This is compared to the typical low-margin back to back oil trading transaction. Higher volume also helps to lower unit fixed cost.

- Contributions from 33%-owned associate Shanghai Pudong International Airport Aviation Fuel Supply Co Ltd (SPIA) grew 61% to US$31mn. SPIA also paid US$23mn to CAO in FY23, 9.5% higher YoY. We expect a higher payout in FY24e after the strong FY23.

The Negative

- Provided for impairment of US$12mn for goodwill (US$3.4mn) and investment in an associate (US$8.7mn), thus lowering net profit.

Source: Phillip Capital Research - 4 Mar 2024

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

THE SINGAPOREAN INVESTOR

Investing in Singapore's Hospitality Scene: A Look at the 5 Listed REITs

2

RHB Investment Research Reports

Food Empire - Expanding Ingredients Capability in Vietnam; BUY

3

RHB Investment Research Reports

ST Engineering - Rolling Forward Our Valuation; Reiterate BUY

4

CEO Morning Brief

Singapore Home Sales Set for Worst Year Since Financial Crisis

5

SGX Market Dialogues

Kopi-C With GuocoLand’s Group CEO: ‘We Have Twin Engines for Growth’

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....