Trader Hub

Far East Hospitality Trust – Mega Events to Drive RevPAR Recovery

traderhub8

Publish date: Thu, 15 Feb 2024, 10:47 AM

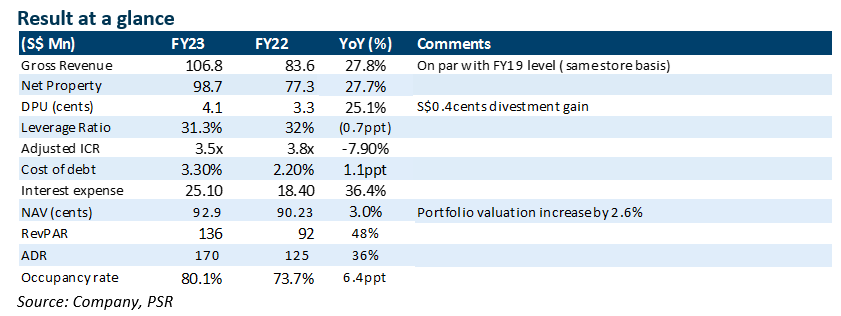

- Gross revenue for FY23 rose by 27.8% YoY to S$8mn on the back of a rebound of hotel revenue of 36%. It was within our expectations. ADR increased by 36.1% YoY to S$170 thanks to rising international visitor arrivals to 71% of pre-COVID level. Occupancy grew 6.3 pp YoY to 80.1%, leading to a 47.8% rise in RevPAR to S$136.

- DPU exceeded our expectation by 7%, surging to 4.09 cents (+25.1% YoY), supported by a higher NPI (+27.7% YoY) and S$8mn distribution of divestment gain of Central Square.

- We reiterate our BUY recommendation with an unchanged DDM-TP of S$0.79 and FY24e-25e DPU forecasts of S$4.35 to S$4.45 cents. As Chinese travelers return supported by 30-day visa-free policy, we expect revenue to rise, backed by the improving occupancy rate. ADR is expected to be maintained due to the line-up of MICE and mega concerts in FY24. FEHT is currently trading at FY24e dividend yields of 6.8% and 0.7x P/NAV

The Positives

+ Recovery on track. ADR exceeded pre-COVID levels, reaching S$170 for FY23, propelled by the recovery in flight capacity. However, RevPAR lags behind, standing at 95% of pre-COVID levels owing to a 9% gap in occupancy rates (FY19: 89.1% vs. FY23: 80.1%). We expect RevPAR to continue trending upward in FY24, with more support from Q2 onwards due to seasonality. Income from variable rental surged by more than six times, surpassing pre-COVID levels by 1% and contributing to 25% of gross revenue amidst the leisure recovery. We expect a decline in contributions from corporate travelers, potentially driving ADR higher in the absence of corporate discounts. Occupancy is forecast to ramp-up in FY24e, thanks to major events such as the Taylor Swift Eras Tour and Singapore Airshow in 2024; current forward bookings appear promising.

+ Potential inorganic growth. FEHT is one of the least geared SREITs with a leverage ratio of 31.3% and debt headroom of c.S$900mn (Gearing at 50%). However, they identify limited growth potential in Singapore due to the tight spread between funding cost and asset yield. There are no near-term plans for acquiring more stake in Sentosa since the ticket size is large and EFR is off the table. The focus remains on low-interest-rate countries such as Japan, with the possibility of acquiring sponsor’s assets in Tokyo and a positive carry of c.2.5%.

The Negative

– Interest rate creeping up. The cost of debt for FY23 was 3.3%, and FEHT expects the rate to increase to c.4% in FY24 when hedges drop off, as only 42.6% of the debt is hedged at a fixed rate.

Source: Phillip Capital Research - 15 Feb 2024

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

THE SINGAPOREAN INVESTOR

Investing in Singapore's Hospitality Scene: A Look at the 5 Listed REITs

2

RHB Investment Research Reports

Food Empire - Expanding Ingredients Capability in Vietnam; BUY

3

RHB Investment Research Reports

ST Engineering - Rolling Forward Our Valuation; Reiterate BUY

4

CEO Morning Brief

Singapore Home Sales Set for Worst Year Since Financial Crisis

5

SGX Market Dialogues

Kopi-C With GuocoLand’s Group CEO: ‘We Have Twin Engines for Growth’

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....