Trader Hub

Keppel Ltd – Energy Buttressed Bottom Line

traderhub8

Publish date: Mon, 05 Feb 2024, 09:59 AM

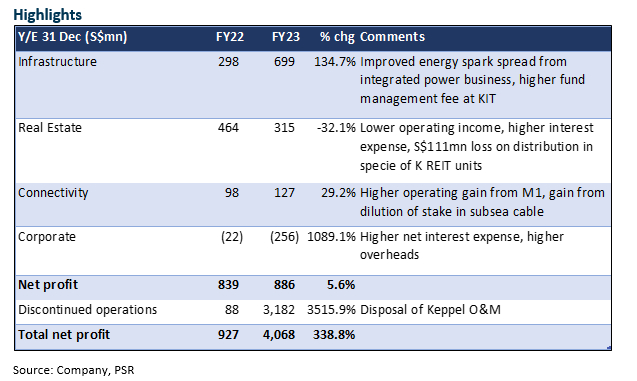

- FY23 core net profit grew 5.6% YoY, in line with our expectations. Recurring income grew 54% to S$773mn, or 88% of net profit. Infrastructure made up 90% of this.

- Growth was underpinned by a higher margin from energy sales, offset by the doubling of interest expense to S$328mn, and S$111mn loss on distribution of K Reit units to Keppel shareholders.

- Energy earnings are sustainable, with 60% of capacity locked in on long-term contracts for more than 3 years. A lower interest rate environment could rejuvenate M&A and fundraising, lifting funds under management. The sale of the rigs in AssetCo could return S$3.1bn to the group, we estimate.

- Downgrade to ACCUMULATE from BUY on recent share price gains. We raised FY24e net profit projections by 0.4%. Our SOTP-derived TP is revised higher to S$7.98 (prev S$7.52), as recurring income takes a bigger share of net profit.

The Positives

+ Integrated power business doubled operating income and margins, benefitted from improved energy spark spread and exit from low-margined legacy contracts. 90% of its capacity is contracted for >1 year, providing visible and sustainable earnings. KIT contributed higher fees after a change in fee structure.

+ M1 grew revenue by 6%, after the acquisition of a Malaysian ICT in late 2022. Key drivers were higher enterprise customer sales (+27%) and total customers (+2%), and recovery of roaming services to 80% of pre-COVID.

The Negatives

– Real estate division was impacted by higher interest expense, lower fair value gains on investment properties and higher overheads at asset management units. The distribution of K Reit units to Keppel shareholders led to a S$111mn loss as the book value exceeded the market value.

– Recurring fee income from fund management fell 5.5% to S$86mn. About S$5bn new funds was raised in FY23. Investors’ appetite was muted amidst rising interest rates and tighter credit conditions. But the pace could pick up in FY24, as recently-acquired Aermont Capital extends its investor reach, and the interest rate environment turns favourable.

– Net gearing rose to 0.9x. Management has an internal net gearing threshold of 1x. Free cash flow was negative S$228mn. Net debt as at end Dec was S$9.7bn, at an average interest cost of 3.75%. Interest expense doubled to S$328mn.

Source: Phillip Capital Research - 5 Feb 2024

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

SGX Market Updates

2

RHB Investment Research Reports

Marco Polo Marine - Higher Capacity To Drive Growth; Maintain BUY

3

Collin Seow Remisier Blog

Baker Hughes: Powering Essential Industries and Your Portfolio

4

THE SINGAPOREAN INVESTOR

5

RHB Investment Research Reports

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....